November 10, 2017

eCobalt SEDAR Files Positive Feasibility Study for the Idaho Cobalt Project; Pre-Tax NPV $176M 7.5%, IRR 25.1%

Economic Summary

Pre-Tax NPV7.5% |

$176.9M |

|

Pre-Tax IRR |

25.1% |

|

Post-Tax NPV7.5% |

$135.8M |

|

Post-Tax IRR |

21.3% |

|

Corporate Tax Rate |

34% |

|

Initial Capital Costs |

$186.7M |

|

Life of Mine (LOM) |

12.5 years |

|

LOM Average Co Sulphate Price (contained Co) |

$26.65/lb |

|

LOM Gross Revenue |

$1.129B |

|

LOM Total Net After Tax Cash Flow |

$331.4M |

|

LOM Average Net Cash Cobalt Production Cost |

$5.05/lb |

|

Pre-Tax Initial Capital Payback |

2.9 years |

|

LOM Cobalt Production (lbs) |

31,767,000 |

|

LOM Copper Production (lbs) |

42,819,000 |

|

LOM Gold Production (oz) |

39,241 |

(Note: All monetary values used in this news release are in Q3 2017 US dollars)

Vancouver, B.C. November 10, 2017 – eCobalt Solutions Inc. (ECS-TSX) (“eCobalt” or the “Company”) is announcing the SEDAR filing of a Feasibility Study Technical Report (“FS”) of the Company’s Idaho Cobalt Project (“ICP”), the only environmentally permitted, primary cobalt project located in the United States (see company news release dated September 27, 2017). The economic model uses a 34% corporate tax rate and a 7.5% discount rate, resulting in an after-tax NPV of $135.8M and an IRR of 21.3% using an average base case price of $26.65/lb for contained cobalt in cobalt sulphate.

The ICP is 100% owned by the Company’s wholly owned subsidiary, Formation Capital Corporation, U.S. The FS was prepared by Micon International (“MI”) in conjunction with SNC Lavalin (“SNC”) both of Toronto, Canada. The FS is based on an underground mine with a target production rate of 800 short tons per day (“tpd”) and a weighted average annual production of 2.4M lbs of cobalt, 3.3M lbs of copper and 3,000 oz of gold over a 12.5 year mine life with an estimated pre-production period of 24 months utilizing a 0.25% cobalt cut-off grade. The FS outlines the production and processing feasibility of ICP as an underground mine and mill, developing the Company’s Ram deposit, located within the Idaho Cobalt Belt outside the town of Salmon, Idaho and the Cobalt Production Facility (“CPF”), a hydrometallurgical refining operation to be located on a railhead in Blackfoot, Idaho. The ICP would be a vertically integrated project designed to produce cobalt chemicals for the rechargeable batteries market in addition to by-products of copper concentrate, copper sulphate, magnesium sulphate and gold. The feasibility recommends the ICP progress through detailed engineering, procurement and construction phases.

Mr. Paul Farquharson, President and C.E.O. of the Company stated: “The filing of our Feasibility Study FS signifies a significant milestone in the development of the ICP. With a Technical Report on file, the Company can now disclose additional details of the project to potential financiers and their due diligence teams to assist in the advancement of the Project through financing and ultimately, construction and production. To that end, our management team has been aggressively pursuing the marketing of the project to potential financiers in North America and abroad. Additionally, potential offtakers have toured the project and as previously announced, pre-construction activities are underway in preparation for project construction and mine development with the intent of recommencing construction in the summer of 2018 contingent upon successful project financing. The near-term aspect of high grade primary cobalt produced in the United States is the essence of the ICP’s main competitive strengths.”

Feasibility Study Description

As previously described, the FS is based on an underground mine with a target production rate of 800 short tons per day (“tpd”) and a life of mine production of 31.8M lbs of cobalt, 42.8M lbs of copper and 39,241 oz of gold. The project has over 12.5 year mine life with weighted average annual production of 2.4M lbs of cobalt, 3.3M lbs of copper and 3,000 oz of gold and an estimated pre-production period of 24 months utilizing a 0.25% cobalt cut-off grade. The economic model uses a 34% corporate tax rate and a 7.5% discount rate, resulting in an after tax NPV of $135.8M and an IRR of 21.3% using an average base case price of $26.65/lb for contained cobalt in cobalt sulphate.

The Company completed a Preliminary Economic Assessment (“PEA”) on March 10, 2015 utilizing the Company’s September 14, 2007 (revised May 19, 2008) feasibility study as a basis. The PEA included the completed environmental permitting process and construction at the mine and mill that was completed from 2011 to 2013 and subsequently placed on care and maintenance in May 2013. The FS utilizes an updated resource, mine model and mine schedule with a feasibility study level of design for the CPF to produce cobalt sulphate. A combined cobalt/copper/gold concentrate is to be produced from the mine and mill and processed at the CPF through hydrometallurgical processing of cobalt and copper bearing sulphides to produce cobalt sulphate heptahydrate which is used in the production of cathodes for rechargeable batteries.

Marketable by-products include copper concentrate, copper sulphate, magnesium sulphate and gold. Gold will be recovered through a gold carbon in leach circuit producing gold-loaded carbon which will be refined at a contract facility to produce doré. The stripped carbon will be returned to the CPF for reuse.

The ICP is 100% owned by eCobalt and there is no underlying royalty on the property. The FS has been compiled in accordance with National Instrument 43-101 guidelines. Readers are strongly encouraged to review the final National Instrument 43-101 Technical Report in its entirety.

Mineral Resource and Reserves

MI updated the estimate of cobalt, copper, and gold resources in a three-dimensional resource wire frame and block model to be used for mine planning, design, and scheduling as part of the FS. MI utilized the previously estimated resources for the Ram deposit (completed by Mine Development Associates for the PEA) supported by their own geostatistical model and reserve criteria. The resulting model moved some PEA level Measured resources into the Indicated category and adjusted grades within the resource categories. Cobalt, copper, and gold reported resources in the FS model are shown in the table below. The stated resource is reported at a cobalt cut-off grade of 0.20% cobalt. There is approximately 34% dilution forecasted in the stope designs with additional dilution applied, by mining method and stope conditions, for over-break. The copper and gold resources and reserves are those resources and reserves carried within the stope blocks which attain the cobalt cut-off grade. No metal value is given to the copper or gold in determining the cobalt resource cut-off. No metal recoveries are applied, as this is an in-situ resource.

Ram Deposit Mineral Resources at 0.2% Co Cut-off

Category |

Resource (Tons) |

Co (%) |

Co |

Au (opt) |

Au |

Cu (%) |

Cu |

|

Measured |

1,725,000 |

0.54 |

18,590 |

0.014 |

24,300 |

0.76 |

26,322 |

|

Indicated |

1,711,000 |

0.64 |

21,988 |

0.017 |

29,900 |

0.71 |

24,111 |

|

M+I |

3,436,000 |

0.59 |

40,578 |

0.016 |

54,200 |

0.73 |

50,436 |

|

Inferred |

1,543,000 |

0.51 |

15,594 |

0.012 |

18,700 |

0.68 |

21,032 |

Ram Deposit Mineral Reserves at 0.25% Co Cut-off

Category |

Resource (Tons) |

Co (%) |

Co |

Au (opt) |

Au |

Cu (%) |

Cu |

|

Proven |

1,987,209 |

0.43 |

17,107 |

0.013 |

25,276 |

0.69 |

27,384 |

|

Probable |

1,674,685 |

0.52 |

17,410 |

0.017 |

28,010 |

0.67 |

22,372 |

|

Total Reserve |

3,661,894 |

0.47 |

34,517 |

0.016 |

53,286 |

0.68 |

49,756 |

Economic Highlights

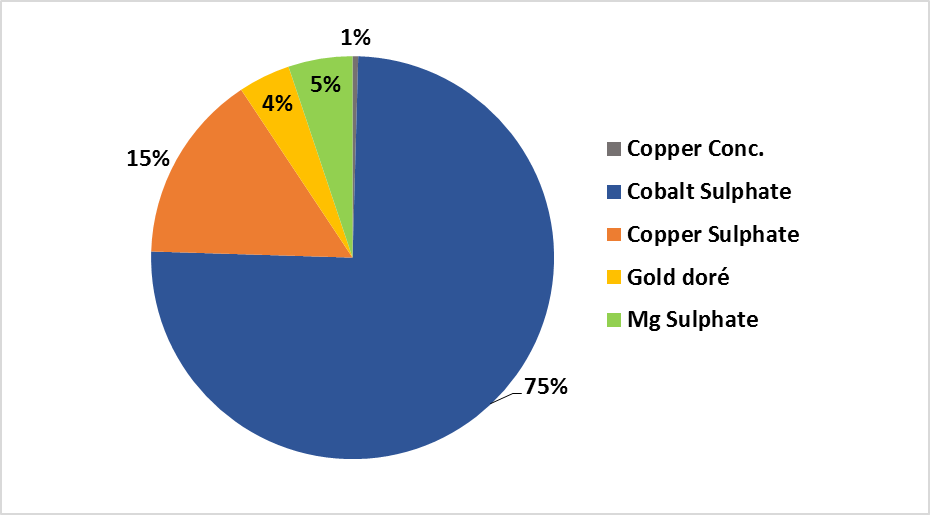

The FS economic model uses a 34% corporate tax rate and a 7.5% discount rate, resulting in an after tax NPV of $135.8M and an IRR of 21.3% using an average price of $26.65/lb of contained cobalt in cobalt sulphate. Gross revenue during the life of mine is estimated to consist of 75% cobalt sulphate, 15% copper sulphate, 5% magnesium sulphate, 4% gold and 1% copper concentrate. A pro forma cash flow was developed using conventional methodology utilizing the base case discount rate, before and after-tax determination of project economics, annual cash flows discounted on an end of year basis with costs estimated in Q3-2017 US dollars.

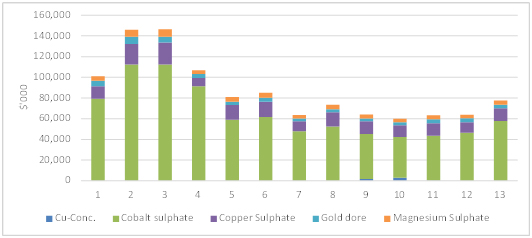

LOM Cobalt Sulphate and By-Product Revenue

By Year through LOM the following chart demonstrates the projected Sales Revenue by Product

LOM Cobalt Sulphate and By-Product Revenue

The total LOM capital and reclamation cost is estimated at $288.1M, including $186.7M for initial capital, $5.8M for long term water treatment bond collateral, and $95.6M in sustaining capital and mine development capital during production over the LOM, reclamation and closure cost. Prior to the deferral of the ICP to care and maintenance status in May 2013 due to depressed market conditions; the Company spent $65.3M on the ICP for earthworks, engineering, and milling equipment including the crushing, ball mill, flotation and filtration circuits, pumps, grizzlies, hoppers, conveyors, etc. These are sunk costs and not included in the remaining initial capital costs.

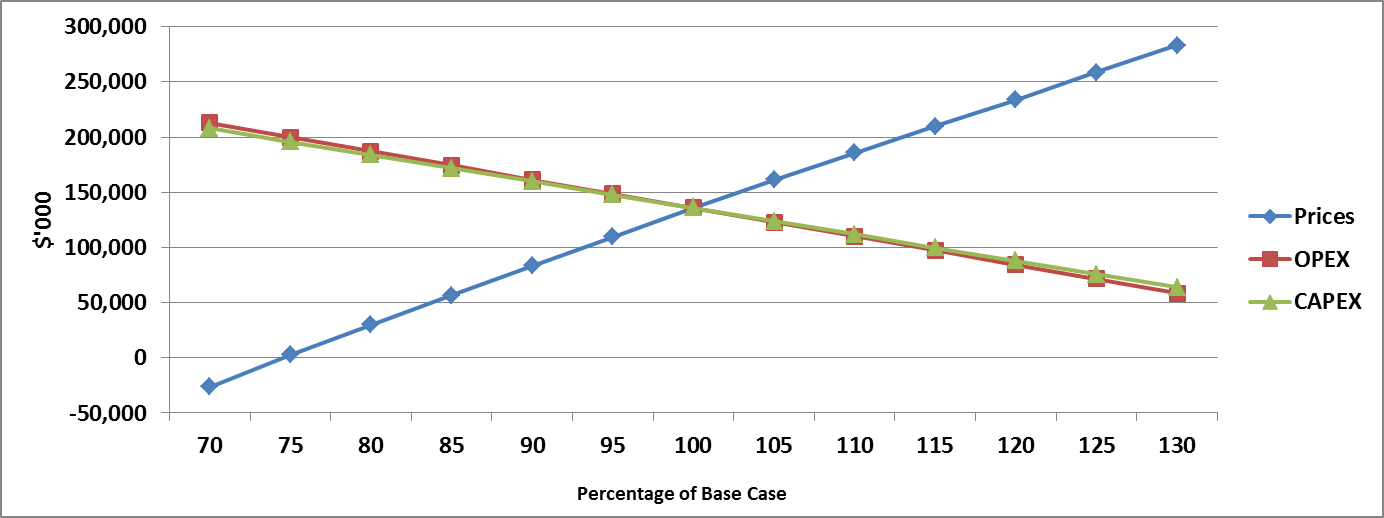

Project sensitivities were evaluated against standard potential variances in the cobalt price, discount rate, capital expenditures, and operating costs. Results of the sensitivity analysis are presented in the following tables and charts.

Cobalt Sulphate Price Forecasted Sensitivity:

Co Sulphate Price: |

$19.50 |

22.50 |

$25.50 |

$26.65* |

$28.50 |

$31.50 |

$34.50 |

|

After-Tax IRR |

10.4% |

15.1% |

19.5% |

21.3% |

23.6% |

27.4% |

31.1% |

|

After-Tax NPV @ 7.5% |

$27.8M |

$73.7M |

$118.4M |

$135.8M |

$162.4M |

$204.0M |

$245.8M |

*Base case

The table above shows that $1.00/lb change in the price of cobalt will lead to a $14.4M change in after tax NPV and 1.3% change in after tax IRR.

Discount Rate Forecasted Sensitivity:

Discount Rate: |

5.5% |

6.5% |

7.5%* |

8.5% |

9.5% |

|

After-Tax NPV using Base Case Prices |

$174.0M |

$154.0M |

$135.8M |

$119.3M |

$104.3M |

*Base case

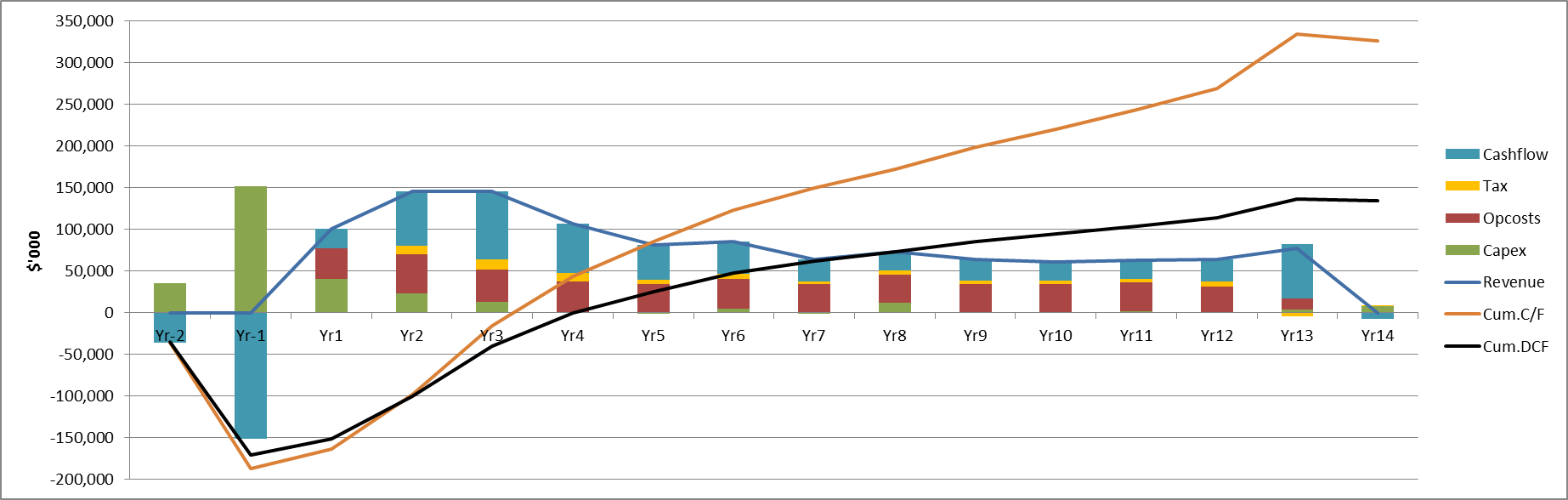

The following table and chart depicts the gross and net cash flow for the project LOM and by year respectively.

Life-of-Mine Cash Flow Summary

Item |

LOM total |

$/t milled |

$/lb Cobalt |

|

Cobalt Sales |

846,837 |

231.26 |

26.66 |

|

Selling Costs |

2,117 |

0.58 |

0.07 |

|

Mining |

196,692 |

53.71 |

6.19 |

|

Mill/Concentrator |

52,494 |

14.34 |

1.65 |

|

Transport |

5,199 |

1.42 |

0.16 |

|

Cobalt Production Facility (CPF) |

149,121 |

40.72 |

4.69 |

|

G&A; |

37,309 |

10.19 |

1.17 |

|

Total Operating Costs |

442,932 |

120.96 |

13.94 |

|

By-product credits |

(282,510) |

(77.15) |

(8.89) |

|

Net Operating Costs |

160,422 |

43.81 |

5.05 |

|

EBITDA |

686,415 |

187.45 |

21.61 |

|

Capital Costs |

288,146 |

78.69 |

9.07 |

|

Net cash flow before tax |

398,269 |

108.76 |

12.54 |

|

Tax |

66,814 |

18.25 |

2.10 |

|

Net cash flow after tax |

331,454 |

90.51 |

10.43 |

Summary of Annual Forecasted Cash Flow

Sensitivity of Estimated After-Tax NPV to Prices (all products), CAPEX and OPEX

Cobalt Market- Growing Demand and Supply Deficit Forecasted (CRU)

The Company commissioned a marketing study with CRU Consulting of London, United Kingdom, to provide data and forecast on cobalt and by-product markets and specifically cobalt sulphate used in rechargeable batteries applications and the ICP’s position within the battery supply chain. The following cobalt marketing information is referenced from the Market Study for the Idaho Cobalt Project September 2017 Report authored by CRU Consulting.

Cobalt consumption has remained strong over the past six years because of stable demand in alloys, established chemical markets and rapid uptake in lithium ion batteries. CRU expects global refined cobalt demand to approach 166,210 tonnes by 2026 (2016 - 96,000 tonnes). Demand is forecast to grow at 6% CAGR in the mid-term spurred on by growing demand for lithium ion batteries. Demand is then expected to increase at CAGR 4.1% in the long-term (2021-2026) as the EV sector matures and the metals sector continues to grow robustly.

Cobalt mine supply is consolidated in a small number of countries and dominated by the Democratic Republic of Congo. The country’s share of global supply is forecast to reach 67% in 2021 despite considerable risks to political stability, infrastructure development and energy supply. Cobalt chemicals supply is dominated by China, the largest importer of cobalt concentrates and hydrometallurgical intermediates. Being located in the United States, the ICP with access to its own mined feedstock, sustainable operating practices following ethical principles is an advantageous position in the current market environment. The ICP has the opportunity to become the reliable and transparent source of cobalt sulphate supply to the domestic market and export markets outside DRC.

Cobalt sulphate demand is rising strongly and is likely to outperform demand for other cobalt chemicals and demand in metallurgical applications in the future. Tightness in both the metallurgical and non-metallurgical sectors will lead to increasing competition for both mined and refined supply helping support prices at or above current levels over the next ten years. Most of this deficit will be felt in the non-metallurgical market, where supply and demand is expected to increase at CAGR 7.0 % and CAGR 7.9 % respectively. This means additional chemical refining capacity will need to be created in the mid-term. Delays in capacity increases could occur as a function of political instability, energy disruption or as a function of falling copper and nickel prices. The global supply of refined chemicals is becoming increasingly prone to mine supply bottlenecks, a major upside risk to cobalt chemical prices.

Based on CRU’s long term real price forecast, the FS uses a weighted average price of $26.65/lb for contained cobalt in cobalt sulphate, which has an average premium of $1.47/lb above 99.3% cobalt price forecast.

Current Activities

Pre-construction activities continue at the ICP Mine and Mill site. These activities include the installation of the main substation and extension of power lines to the portal bench, the concentrator pad, and the water retention ponds and control wells. Mobilization of the crushers to the mill site for early spring resumption of waste pad construction has been completed.

Project Opportunities

There are significant opportunities that could improve the economics of the ICP. Including those opportunities typical to all mining projects, such as changes in metal prices, exchange rates, etc., there are additional opportunities that exist. The mineral resource has not been fully delineated and there is an excellent opportunity to expand this resource. As a result, the Company initiated a targeted drilling program, in consultation with MI. The first drill hole completed has successfully intercepted additional mineralized material within a deeper Indicated zone to the South of the deposit. Pending the receipt of assays, the results of this drill hole have the potential to immediately increase the indicated mineral resource. In addition, over a dozen potential targets have been identified in the immediate area within the claim block of the ICP. Four of these have been drill tested with several intercepts exceeding the current cut-off grade. There is also potential to add additional resources from the nearby Black Pine property owned by the Company which potentially could provide additional feed for the ICP mill.

There is an opportunity for the mine to process higher grade material for short durations through the optimization of the mine plan and sequence production to capitalize on market conditions. Opportunities for CPF capital and operating cost improvements exist through optimization studies during detailed design. There is potential to increase overall recoveries and obtain better shipping and handling terms through formal negotiations in the future and to incorporate offtake and/or streaming agreements on some or all of the products to be produced.

FS Risks

The most significant potential internal risks associated with the ICP are uncontrolled dilution, lower metal recoveries than those projected, operating and capital cost escalations, unforeseen schedule delays, and the ability to raise sufficient financing to execute the project. The central external project risks are product prices and markets. These risks are common to most mining projects, many of which can be mitigated with adequate engineering, planning and pro-active management.

Conclusions

MI and SNC have concluded that the FS contains adequate detail and information to support the positive FS outcome shown for the ICP. Standard industry practices, equipment and design methods were used in the FS. MI and SNC further concluded that the ICP contains a viable cobalt and base metal resource that can be successfully mined by underground methods and recovered to concentrate with conventional milling processes. Using the assumptions contained in the FS; in the professional opinions of MI and SNC, the project economics merit consideration by eCobalt to proceed to the project financing and execution stage. To date the Qualified Persons, in accordance with National Instrument 43-101, are not aware of any fatal flaws for the ICP. The advancement of the ICP towards production is contingent upon financing.

Moving Forward

The positive results of the FS have given Management and the Board of Directors a clear mandate to move the ICP towards project financing and development. Management has conducted project marketing discussions with potential finance and off-take partners who have executed non-disclosure agreements with the Company and begun due diligence reviews and testing of product samples.

Independent of the FS, Management’s is evaluating a variety of opportunities for the ICP in cooperation with the FS engineers and in response to offtake discussions.

Preparation of the ICP mine and mill site for construction activities, expected to commence in earnest next year with successful mine financing in place, continues with access road upgrades, existing facilities maintenance, preparation of temporary power for construction, and approved water discharge line maintenance. At the CPF located in Blackfoot, ID, the existing pre-purchased building has been transported to the site.

Concurrent with the above activities, Management also plans on pursuing the numerous opportunities for project enhancement.

The Qualified Persons as defined by National Instrument 43-101 responsible for the FS and this news release are listed below:

|

Qualified Person |

Organization |

Overall Responsibilities |

|

Chris Jacobs CEng MIMMM |

Micon International Limited |

Project Economics and Cost Estimates. |

|

Charley Murahwi P.Geo. FAusIMM |

Micon International Limited |

Geology and Mineral Resource Estimates |

|

Barnard Foo P.Eng. |

Micon International Limited |

Mining and Reserve Estimates |

|

Richard Gowans P.Eng. |

Micon International Limited |

Metallurgy and Process Design |

|

David Makepeace M.Eng. P.Eng. |

Micon International Limited |

Environmental Engineering |

| Jane Spooner | Micon International Limited | Minerals Markets |

|

E.R. (Rick) Honsinger, P.Geo. |

eCobalt Solutions Inc. |

Review and approval of the contents of this news release |

About eCobalt Solutions Inc. (www.ecobalt.com)

eCobalt Solutions is a well-established Toronto Stock Exchange listed company committed to providing ethically produced, environmentally sound, battery grade cobalt salts, essential for the rapidly growing rechargeable battery and renewable energy sectors, made safely, responsibly, and transparently in the United States.

eCobalt Solutions Inc.

“J. Paul Farquharson”

J. Paul Farquharson

President & CEO

For further information please contact:

eCobalt Solutions Inc., 1810 – 999 West Hastings Street, Vancouver, BC, V6C 2W2

Tel: 604-682-6229 - Email: [email protected] – Web: ecobalt.com

Cautionary Statement on Forward Looking Statements

This news release contains “forward-looking statements” within the meaning of applicable Canadian securities legislation. Statements in this news release pertaining to expected financings, filings, uses of proceeds or project completion dates are forward-looking statements. These forward-looking statements are based on assumptions and address future events and conditions and are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking statements.

Such projections are and will inevitably always be dependent on assumptions about future mineral prices and development costs which will be subject to fluctuation due to global and local economic and industry conditions. Further information regarding risks and uncertainties which may cause results to differ from those contained in forward-looking statements is included in filings by the Company with securities regulatory authorities and is available at www.sedar.com. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Although the Company has disclosed that the Idaho Cobalt Project remains the sole, near term, environmentally permitted, primary cobalt deposit in the United States and offers a unique potential for North American consumers to secure an ethically sourced, environmentally sound supply of battery grade cobalt chemicals, there is no guarantee that the Company will attain commercial production of such cobalt chemicals for use in the rechargeable battery sector. Accordingly, readers should not place undue reliance on forward-looking statements. The Company does not undertake to update any forward-looking statements that are contained herein, except in accordance with applicable securities laws.

The statements contained in this news release in regard to eCobalt Solutions Inc. that are not purely historical are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including eCobalt Inc.’s beliefs, expectations, hopes or intentions regarding the future. All forward-looking statements are made as of the date hereof and are based on information available to eCobalt Solutions Inc. as of such date. It is important to note that actual outcome and the actual results could differ from those in such forward-looking statements. Factors that could cause actual results to differ materially include risks and uncertainties such as technological, legislative, corporate, commodity price and marketplace changes.

September 27th, 2017, eCobalt Announces Positive Results from the Feasibility Study on the Idaho Cobalt Project

November 15th, 2017, eCobalt Management Update on the Idaho Cobalt Project’s Marketing, Construction and Project Optimization